Gold Bangles Design for Daily Use With Price

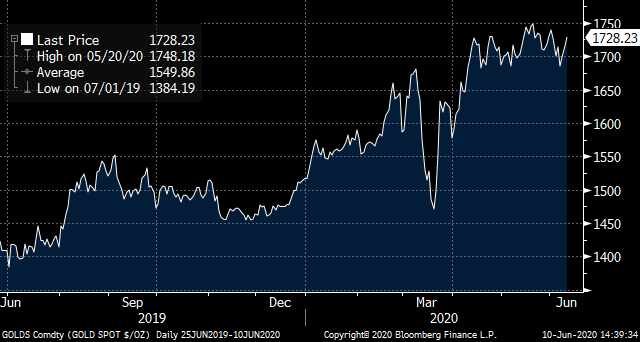

Gold prices in the spot market are up by 12% year to date. That continues to compare very well to the general stock market in the S&P 500 which is down in price by 1.3%. And even though the U.S. bond market is positive by 5.2% as measured by the Bloomberg Barclays U.S. Aggregate Index — gold is still one of the champion assets so far this year.

Source: Chart by Bloomberg

Spot Gold Prices to Date

I got on board the gold train back on June 25, 2019. And it was the first gold recommendation in my professional career as a newsletter editor — ever. I've always viewed gold as an odd investment. It doesn't generate yield in most market forms, so there is a cost to hold it. And I've never viewed it as a form of currency as you can't really spend it without taxable events under IRS rules.

My reasons for my call for a rise in gold rested in two specific developments. The first was low to lower U.S. interest rates. The second was a U.S. dollar that was under control and not set to soar.

Gold is generally priced in U.S. dollars. So, a rising dollar in a static gold market means that the price for gold would fall. And conversely, a falling dollar would make for a better environment for gold prices. And even if the dollar just was neutral, it wouldn't provide a headwind for gold.

But short-term interest rates are the real driver for gold prices. Holding gold has two primary costs that include storage and opportunity or finance costs. Let's focus on opportunity cost. Since gold doesn't pay a yield, there is the cost of lost interest given up each day that gold is held. And for many institutional gold investors — who also will finance gold — interest rates directly impact the cost of holding gold.

The lower the interest rates, the better gold will fare. This is seen in the graph showing one-month U.S. Treasury yield and the spot price of gold from June 2019 to date. There is and has been an inverse relationship between gold and interest rates.

Source: Chart by Bloomberg

Spot Gold (Gold) and 1-Month U.S. Treasury Yield (White)

What Is the Federal Reserve Doing to Gold Prices?

Back last year, I saw rates heading lower thanks to low inflation and changes in the Federal Reserve's monetary policy. The Personal Consumption Expenditure (PCE) index was below the Fed's target rate of 2%. It was slipping.

In response, the Fed began to reverse its policies. This started to move short-term U.S. rates lower.

The Fed kept moving to easier policy in the credit markets last year. And of course, the Fed is all-in and then some this year driving rates ever closer to zero. The PCE will remain low for the foreseeable future and the Fed is going to work like the Dickens to keep rates on the floor. Gold is benefitting as it makes for a cheaper store of value with low interest rates.

Then outside the U.S., interest rates and bond yields are in negative territory, meaning that banks are charging for deposits and bond buyers are accepting built-in costs to buy and own bonds.

The overall amount of negative-yielding debt in U.S. dollar terms has been surging since just March. It has gone from $7.7 trillion to $12.1 trillion. That makes gold all the more attractive to store value over deposits or government bonds outside the U.S. that offer negative yield.

Source: Chart by Bloomberg

Global Sum of Negative Yield Debt in U.S. Dollar Terms

And the U.S. dollar is continuing to come off recent highs. The Bloomberg U.S. Dollar Index has been dropping, making gold all the better in U.S. dollar terms. I see the dollar down for now and at worst remaining neutral.

Source: Chart by Bloomberg

Bloomberg U.S. Dollar Index (White) and Spot Gold (Gold)

Lower U.S. interest rates, negative yield and interest rates outside the U.S. and a benign U.S. dollar have been and will keep driving gold higher.

It's All About Gold Inventories

Now, the conditions last June were great for gold. And they've only gotten better recently, which supports my call to buy gold now. But there are some other reasons gold is likely to do well in the near term.

Physical gold supplies have been under stress. The demand for physical gold for both allocated and unallocated gold positions, as well as for bullion coins, has driven spreads between spot gold and physical gold way higher than normal.

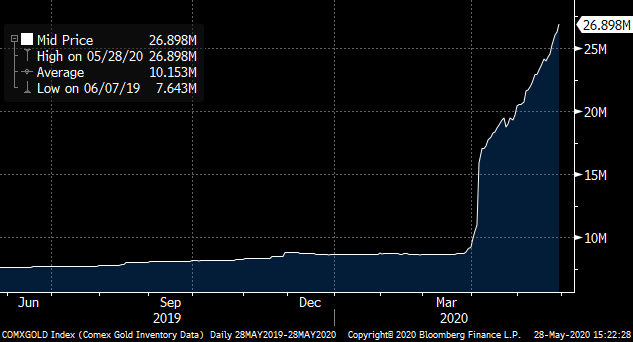

Gold inventories for the CME in New York have been spiking. This comes as the market plays catch-up for required settlements for futures contracts as well as for deliveries for customers taking physical gold.

Source: Chart by Bloomberg

Comex Gold Inventory

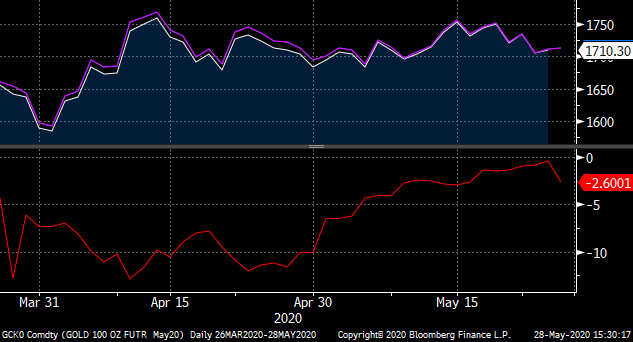

This spike in inventories has come with a surge in shipments flown into New York — amounting to more than 17 million ounces in just the past five weeks. And as contracts rolled over from May to June, the discount didn't close properly. Why? the surge in inventories reached a very short-term glut.

Source: Chart by Bloomberg

CME Gold May (White) June (Purple) and Spread (Red)

There was a buying opportunity then, and there's one now, as settlements and the inventory match up is getting resolved. This makes for more normalized pricing which should head higher based on the fundamentals noted above.

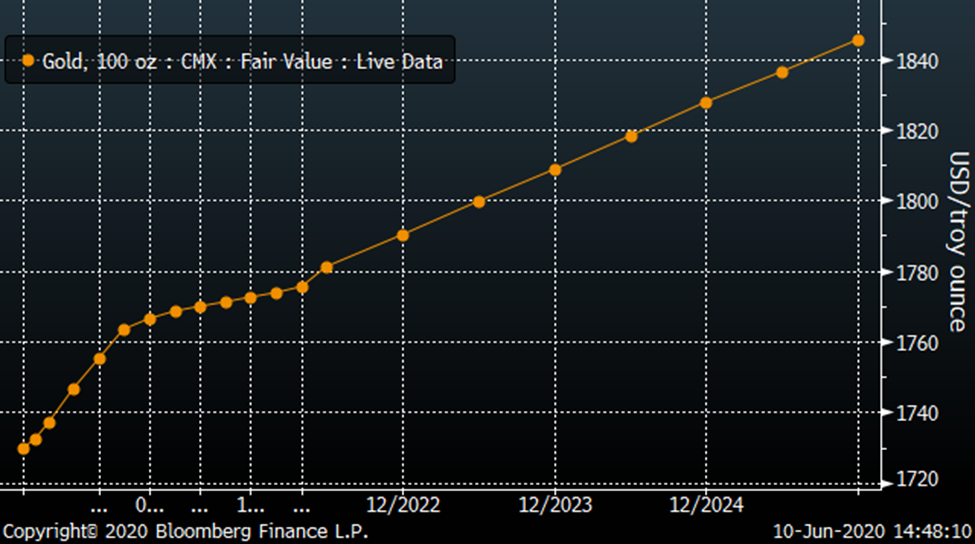

The forward curve for CME (New York) gold contracts is in contango — meaning that over time, longer contracts are higher in price. In other words, the futures price of gold is higher than the spot price today.

Source: Chart by Bloomberg

CME Forward Curve for Gold Contracts Source

With the U.S. Treasury yield curve very flat out five years, I see the forward curve for gold futures in spot prices as supporting higher gold over the coming months. Storage normalization in the physical market is aiding this happening over the coming weeks.

What Does Gold Look Like Across the Pond?

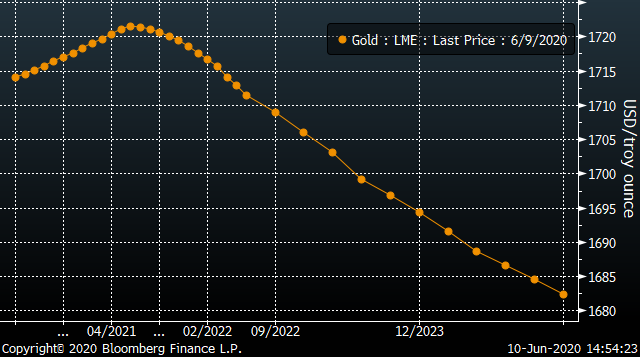

Meanwhile, in London, the other major market for gold and gold futures is the London Metals Exchange (LME). The LME has a forward price curve for contracts which is in backwardation — meaning that longer-term contracts are at discounts to shorter-term contracts.

Source: Chart by Bloomberg

LME Gold Futures Contracts Forward Curve

I see this condition in London reflecting the physical supplies that were shifted in haste to New York — the move has left London in shorter supplies for near-term contracts. This too will aid demand for gold neat term. And the discount of London (LME) to New York (CME) should close over the coming weeks as the markets catch up on physical supplies and deliveries.

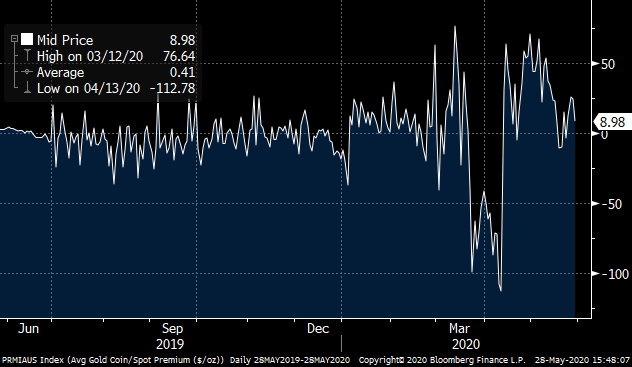

Meanwhile, let me show you the premium of bullion coins to spot gold. The premium to bullion coins over spot gold tends to be modest with the average for all of 2018 through 2019 running at $4.06 per ounce. But during the quest for cash in March of this year it plunged to a discount of $112.78 in early April. It then spiked into the $50 range with shortages that emerged just like in the physical gold market.

Source: Chart by Bloomberg

Average Gold Coin/Spot Premium

The spread has come down measurably, making for a normalizing market. And dealers that I know confirm this as they have customers that were waiting for delivery and to be able to buy more.

I see that pent-up demand is going to flow through to higher prices for gold bullion coins — also supporting overall higher gold prices.

Investors Are Chasing Gold Through ETFs

Then we come to another source of gold supply imbalance. Gold exchange-traded fund inflows in the U.S. have hit a year-to-date record of over $18.5 billion. The leading — and largest — ETF, the SPDR Gold Shares ETF (NYSEARCA: GLD ) has pulled in over $12 billion.

This continued participation by individuals and institutional investors should continue to drive gold prices higher on higher demand. Perhaps it's also being reflected in the spread between CME and LME market prices.

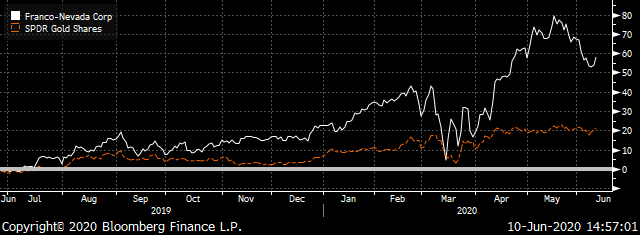

The Best Way to Buy Gold: Franco-Nevada (FNV)

Now, I've written in my Profitable Investing that you should not buy GLD and instead focus your attention on my Franco-Nevada (NYSE: FNV ) company. FNV is not a mining company, but rather owns interests in gold and other mineral production.

It yields 0.79% against GLD's zero yield — and also avoids GLD's expense ratio of 0.4%.

The return of FNV continues to outpace gold and GLD. It has returned 58% since my recommendation last year compared to GLD's meager 21%.

Source: Chart by Bloomberg

Total Return FNV (White) and GLD (Red)

And there is one more reason not to buy GLD. Like other gold ETFs, it is considered a grantor trust under IRS rules. This means it is subject to tax rates of 28%, even on longer-term holdings.

Bottom line, gold should fare well on fundamentals of lower interest rates and a lower, or at least compliant, U.S. dollar. And the recent gyrations in the futures and physical markets for gold are providing an additional buying opportunity right now.

And with FNV, you also get the dividend yield without added costs as you do with GLD.

Neil George was once an all-star bond trader, but now he works morning and night to steer readers away from traps — and into safe, top-performing income investments . Neil's new income program is a cash-generating machine … one that can help you collect $208 every day the market's open . Neil does not have any holdings in the securities mentioned above.

Gold Bangles Design for Daily Use With Price

Source: https://investorplace.com/2020/06/heres-why-gold-prices-are-headed-higher/

0 Response to "Gold Bangles Design for Daily Use With Price"

Post a Comment